Court Orders Shoprite Uganda to Pay Shs 1.3bn in VAT Arrears

Shoprite Uganda was acquired by Carrefour

Kampala, Uganda | The Tax Appeals Tribunal (TAT) has ruled that Shoprite Checkers (U) Limited is liable to pay Shs 1,354,624,690 in Value Added Tax (VAT) to the Uganda Revenue Authority (URA), following a protracted dispute over undeclared sales for the 2016 and 2017 financial years.

The tribunal, however, directed the parties to reconcile a contested Pay-As-You-Earn (PAYE) liability of Shs 58.9 million by July 15, 2025.

In its recent ruling, the three-member panel chaired by Siraj Ali found that Shoprite had failed to disprove URA’s claim that it under-declared sales by including internal stock transfers in its VAT-exempt computations.

The tribunal rejected Shoprite’s explanation that the disputed sales arose from inter-divisional transactions between its Freshmark Division and Supermarket Division, which it claimed involved only unprocessed agricultural products and therefore exempt from VAT.

“Contrary to the assertion by the Applicant, the items transferred…were not entirely composed of unprocessed agricultural products,” the tribunal ruled. “Some of the items were standard rated processed products which were not exempt from VAT.”

URA had based its assessments on discrepancies between Shoprite’s declared VAT sales and the figures used to calculate franchise fees—figures which included internal stock transfers.

Shoprite argued the discrepancy was due to an accounting error following the departure of its finance manager and said the franchise fees had been mistakenly calculated using internal transfers that should not have counted as gross sales.

But the tribunal dismissed that explanation as implausible and inconsistent with corporate accounting standards and internal controls, particularly given that the franchise fee error recurred in two successive years.

“It is hard to believe…that no other person in the Applicant’s finance department was aware that in computing the annual franchise fees, it was essential to exclude the inter-divisional sales from the total sales,” the ruling stated.

Steps

The tribunal also faulted Shoprite for failing to take corrective steps such as amending its tax returns, requesting refunds from the franchisor, or providing sufficient proof that the goods transferred internally were VAT-exempt.

Sample invoices submitted in evidence listed taxable processed products such as Snack Mixes and Dried Fruit Flakes, undercutting the supermarket’s defense.

On the disputed PAYE liability of Shs 58.9 million, the tribunal found that the matter revolved around taxable sundry benefits such as rent, school fees, and utilities provided to expatriate staff.

Although both parties agreed the benefits were taxable, Shoprite insisted it had already accounted for the tax obligations.

“The dispute…can be disposed of through reconciliation,” the tribunal ruled, instructing both parties to reconcile the PAYE dispute and file a report by July 15, 2025.

The tribunal awarded URA three-quarters of the costs in the application.

The ruling highlights the growing scrutiny on multinational corporations operating in Uganda and the importance of consistent accounting practices, especially in sectors like retail where internal transactions can obscure tax liabilities.

Shoprite, which exited the Ugandan retail market in 2021, is still liable for tax audits and obligations incurred during its operational years.

Air Serv Launches Scheduled Entebbe–Arua Flights to Boost Trade and Tourism

Ultimate Uganda

Air Serv Launches Scheduled Entebbe–Arua Flights to Boost Trade and Tourism

Ultimate Uganda

Masaka could lose chance to host regional industrial park

Ultimate Uganda

Masaka could lose chance to host regional industrial park

Ultimate Uganda

GOLD SCAM SHOCKER! Mestil Hotel Resident Canadian Remanded Over Alleged Sh5.6Bn Fake Gold Con That Fleeced Somali Defence Minister

Ultimate Uganda

GOLD SCAM SHOCKER! Mestil Hotel Resident Canadian Remanded Over Alleged Sh5.6Bn Fake Gold Con That Fleeced Somali Defence Minister

Ultimate Uganda

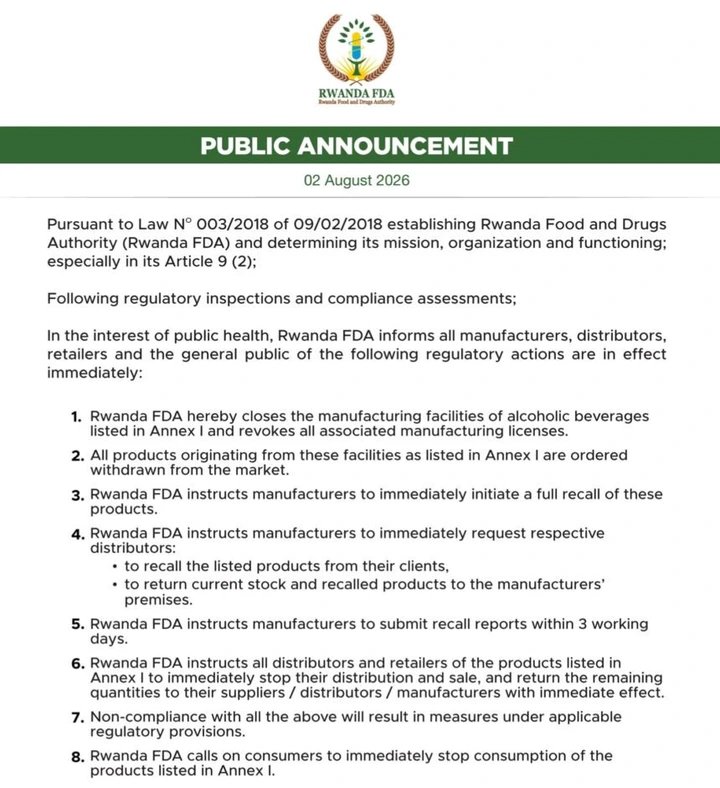

Rwanda Shuts Eight Liquor Factories, Recalls Dozens of Alcohol Brands

Ultimate Uganda

Rwanda Shuts Eight Liquor Factories, Recalls Dozens of Alcohol Brands

Ultimate Uganda

0 Comments