How Mobile Money Taxes Are Squeezing Life Ouf of Small Businesses

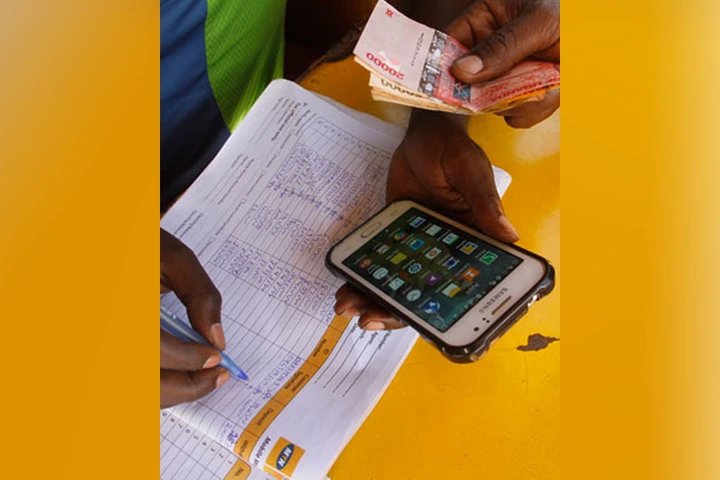

Rising mobile money transaction and withdrawal charges are increasingly eating into the profits of small businesses in Uganda, with traders and MSMEs warning that the high cost of digital transactions could slow the country’s push toward a digital economy.

Mobile money has revolutionized the way Ugandans transact, offering speed, convenience, and safety in financial exchanges. With transaction volumes hitting an impressive Shs195.5 trillion in 2025, according to MTN Uganda’s full-year results, the platform has become the backbone of daily commerce.

However, beneath this success lies a growing concern—rising transaction and withdrawal charges that are increasingly burdening small businesses.

For many micro, small, and medium enterprises (MSMEs), mobile money is no longer optional; it is essential. Yet the cost of using it is slowly eroding profits and threatening business sustainability.

In Nakasero Market, fruit vendor Richard Katongole represents a new generation of digitally savvy traders. Leveraging social media platforms like TikTok, Katongole has expanded his customer base beyond the physical market, offering delivery services and reaching clients across Kampala.

“Social media has helped me grow my business. I now get customers I would never meet physically. I take pictures of everything sold in the market and post them on TikTok, and I receive responses from people ordering bananas, pineapples, and other products,” Katongole explains.

“But most of them pay through mobile money, and the charges are too high. Every withdrawal reduces what I actually earn.”

Katongole notes that while digital tools have opened new opportunities, the associated transaction costs are steadily eating into his margins, making it harder to reinvest and grow his business.

His experience mirrors that of Namuwaya Janet, who runs a crafts and decoration business largely driven by online orders.

For her, mobile money is central to receiving payments, but the increasing charges are becoming a deterrent.

“Mobile money is fast and secure, but it’s becoming expensive to rely on it every day,” Namuwaya says.

“Sometimes I feel like I lose too much just accessing my own money.”

She adds that the rising costs have forced her to reconsider how she receives payments, despite the risks and inefficiencies of alternative methods.

While the government continues to champion digitization as a pathway to economic growth, stakeholders argue that the current cost structure undermines this goal.

John Walugembe, Executive Director of the Federation of Small and Medium Enterprises (FSMEs), emphasizes that digitization has already proven its value among Ugandan businesses.

“About 60% of MSMEs that digitize record increased sales, profits, and market reach,” Walugembe says.

“They use smartphones to market their products, engage customers, manage suppliers, and provide feedback efficiently.”

However, he warns that the benefits of digitization risk being overshadowed by policy and tax constraints.

“Our tax regime sometimes lags behind innovation,” he explains. “Taxes on smartphones make them less affordable, and mobile money charges have become a real pain point for businesses trying to go digital.”

Walugembe suggests that targeted policy adjustments could unlock further growth in the sector.

“A removal of import tariffs on entry-level smartphones would increase access,” he proposes.

“At the same time, reducing mobile money taxes to around 0.25% or removing them entirely would be a strong incentive for MSMEs to fully embrace digital platforms.”

For traders like Katongole and Namuwaya, these policy discussions are not abstract—they reflect daily struggles. Each transaction fee and each withdrawal charge directly impacts their bottom line.

Despite the challenges, mobile money remains the preferred mode of transaction for many due to its security and efficiency.

However, without intervention, stakeholders warn that high costs could slow the momentum of digital adoption among small businesses.

As Uganda continues its push toward a digital economy, MSMEs are calling for a more supportive environment—one where innovation is not penalized by high operational costs.

For now, traders can only hope that policymakers will listen and act, ensuring that the tools designed to empower businesses do not instead become a barrier to their growth.

Uganda Securities Exchange Earns AA Credit Rating in First Independent Assessment

Ultimate Uganda

Uganda Securities Exchange Earns AA Credit Rating in First Independent Assessment

Ultimate Uganda

Stanbic Bank loses bid to sell mortgaged property after dispute over spousal consent

Ultimate Uganda

Stanbic Bank loses bid to sell mortgaged property after dispute over spousal consent

Ultimate Uganda

Why Speke Resort Munyonyo has become Africa’s premier conference and diplomacy destination

Ultimate Uganda

Why Speke Resort Munyonyo has become Africa’s premier conference and diplomacy destination

Ultimate Uganda

Kabale Beekeepers Receive Shs26.8M Equipment to Boost Honey Production

Ultimate Uganda

Kabale Beekeepers Receive Shs26.8M Equipment to Boost Honey Production

Ultimate Uganda

0 Comments