Withholding Tax Exemption Returns to Six Months: What It Means for Businesses

withholding tax exemption allows qualifying businesses to receive income without deductions at source, improve cash flow management, and reduce administrative burden related to tax credits and reconciliations.

The Uganda Revenue Authority (URA) has officially announced the opening of applications for Withholding Tax (WHT) exemption for the period July to December 2026, marking a notable shift in policy that businesses should not ignore.

For many compliant taxpayers, this announcement is more than just an administrative notice; it signals a return to a six-month exemption cycle, moving away from the 12-month exemption period that had become the norm in recent years.

This change, while subtle on the surface, carries significant implications for business cash flow, compliance discipline and tax planning strategies.

Understanding Withholding Tax exemption

Withholding tax is typically deducted at source on certain payments such as supplies, professional services, and contracts.

While it is not necessarily a final tax, it directly affects cash flow, as businesses must wait to offset or claim it through their Income Tax returns.

A withholding tax exemption allows qualifying businesses to receive income without deductions at source, improve cash flow management, and reduce administrative burden related to tax credits and reconciliations.

For growing businesses, especially those operating on tight margins or large contracts, this exemption can be the difference between liquidity and strain.

From 12 months back to 6 months: A strategic shift

Historically, URA operated a six-month withholding tax exemption cycle, requiring businesses to apply twice a year. Over time, this was revised to a 12-month exemption period, giving compliant taxpayers longer relief and reduced administrative pressure.

However, the latest public notice confirms a reversion to the six-month cycle.

What does this mean?

Businesses will now need to apply more frequently

Compliance will be monitored more closely

The window for maintaining eligibility becomes shorter and stricter

This shift suggests a move by Uganda Revenue Authority (URA) towards enhanced compliance monitoring and accountability.

Rather than granting long-term exemptions, the Authority is creating a system where businesses must continuously demonstrate compliance.

Why this matters for businesses

This change introduces both opportunities and responsibilities.

1. Increased compliance discipline

With a shorter exemption period, businesses must now keep records consistently update, ensure timely filing of returns and maintain continuous tax compliance.

There is less room for error, as non-compliance within the six-month period can easily affect eligibility for the next cycle.

2. Cash flow planning becomes critical

Businesses that rely on exemptions to manage liquidity must now plan around shorter exemption windows, avoid disruptions when exemptions expire, and ensure timely re-application.

Failure to secure an exemption on time could result in unexpected withholding, affecting operations.

3. More frequent interaction with URA systems

The application process is fully digital via the URA portal. With the six-month cycle:

Businesses must engage more regularly with URA systems and the internal tax teams must stay proactive

This reinforces the need for structured tax management systems within businesses.

The compliance threshold

One of the most critical aspects of the new application process is the minimum tax contribution requirement.

To qualify for withholding tax exemption, businesses must demonstrate that they have paid a certain level of taxes over the past period:

Small taxpayers: At least Shs100 million

Medium taxpayers: At least Shs200 million

Large taxpayers: At least Shs500 million

This requirement is significant because it shifts the conversation from: “Are you compliant?” to: “Are you meaningfully contributing to the tax system?”

What this means

Businesses must now ensure that their declared income aligns with actual operations, taxes paid reflect realistic business activity and there is no underreporting or aggressive tax positions. This is a clear signal that URA is prioritising substance over form.

Other compliance requirements

Beyond the revenue contribution threshold, URA has outlined a comprehensive compliance checklist that businesses must meet:

1. Accurate and up-to-date registration

Business details must be current

Directors and associates must have updated information

2. Complete and accurate tax returns

All returns must be filed

Income tax returns for the last three years must be submitted

Compliance with electronic invoicing systems where applicable

3. Full payment of taxes

There must be no outstanding tax liabilities and any disputes must be properly managed or supported.

4. Director-level compliance

Directors must be compliant across all income sources.

5. No ongoing investigations or unresolved issues

Any ongoing investigations must be cleared and outstanding issues with customs or domestic taxes must be resolved.

A broader message from URA

Looking at these requirements collectively, a clear message from URA emerges: Withholding tax exemption is no longer just a compliance benefit—it is a reward for structured, transparent, and disciplined businesses.

URA is saying: Compliance must be consistent, not occasional. Tax contribution must be visible and measurable. And systems must be aligned with declarations.

Strategic considerations for businesses

Given these developments, businesses should take a more strategic approach to withholding tax exemption.

1. Do not treat it as routine

Each application should be approached as a compliance audit of your business.

2. Align systems early

Ensure that Accounting records match tax filings, electronic systems reflect actual transactions and documentation supports all declarations

3. Review tax position regularly

Do not wait for the application window. Conduct periodic reviews. Identify gaps early and correct inconsistencies.

4. Plan for transition periods

Anticipate: Expiry of exemption, delays in approval and temporary withholding.

Shift towards continuous compliance

From a professional standpoint, this move back to a six-month exemption cycle reflects a broader shift in tax administration:

From periodic compliance to continuous compliance.

Tax authorities are increasingly leveraging data, systems, and real-time monitoring. In such an environment, compliance is not an annual event but an ongoing process embedded in business operations.

Businesses that recognise this early will not only qualify for exemptions but will operate with greater confidence and stability.

Final thought

Withholding tax exemption remains a powerful tool for improving business cash flow and reducing administrative burden.

However, under the current framework, only structured, compliant, and transparent businesses will consistently benefit.

“The shift has already happened. The question is—are you ready for it”?

GOLD SCAM SHOCKER! Mestil Hotel Resident Canadian Remanded Over Alleged Sh5.6Bn Fake Gold Con That Fleeced Somali Defence Minister

Ultimate Uganda

GOLD SCAM SHOCKER! Mestil Hotel Resident Canadian Remanded Over Alleged Sh5.6Bn Fake Gold Con That Fleeced Somali Defence Minister

Ultimate Uganda

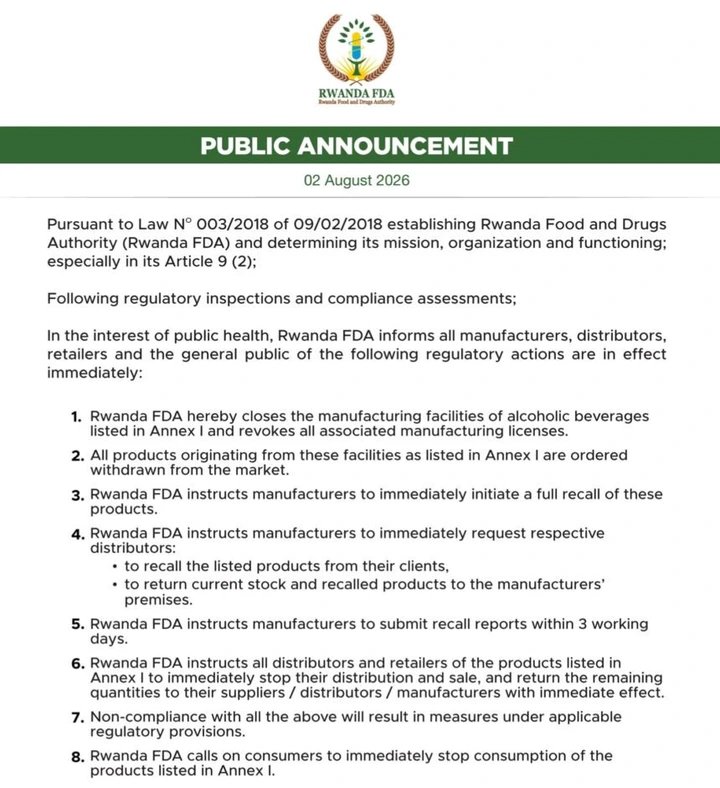

Rwanda Shuts Eight Liquor Factories, Recalls Dozens of Alcohol Brands

Ultimate Uganda

Rwanda Shuts Eight Liquor Factories, Recalls Dozens of Alcohol Brands

Ultimate Uganda

Bunyoro Leaders Demand Greater Local Content Benefits from Oil and Gas Projects

Ultimate Uganda

Bunyoro Leaders Demand Greater Local Content Benefits from Oil and Gas Projects

Ultimate Uganda

Umeme Share Sheds 85% Value ahead of Loss Announcement

Ultimate Uganda

Umeme Share Sheds 85% Value ahead of Loss Announcement

Ultimate Uganda

0 Comments